People often wonder about the best way to transfer property to family in Ontario without creating unnecessary tax or probate issues. Transferring property to family in Ontario is something many homeowners consider, often in the middle of a conversation rather than at the beginning. Understanding how to transfer property effectively can save families from potential pitfalls.

A seller discusses putting a child on the title. Help for the buyer’s purchase could come from their parents. A homeowner inquires about methods to avoid probate later.

It sounds simple. Keep the property in the family and reduce the costs.

When families decide to transfer property, they should consider the implications of their choices. It is essential to explore how to transfer property while maintaining control and minimizing taxes.

It is not simple.

No method avoids tax, probate, or loss of control. Every option shifts cost, timing, or risk. Most problems come from focusing on one piece and ignoring the others.

When you choose to transfer property, consider the potential benefits and drawbacks to your family’s situation.

In Ontario, understanding the costs, like taxes and probate, helps you feel more confident and in control of your decisions, avoiding future surprises.

Understanding these aspects of how to transfer property can lead to better decision-making.

What actually drives the cost

Three things matter: capital gains tax, probate, and land transfer tax

It is critical to weigh these factors carefully when you aim to transfer property.

Capital gains tax is the one that catches people off guard. The Canada Revenue Agency treats the transfer as if the property sold at fair market value, even if no money changes hands, as its guidance on transfers of capital property outlines.

A simple example makes this clearer. A property owner has a $500,000 gain if they purchased a property for $300,000 and it is now worth $800,000. The government will tax a portion of that gain in the year of transfer if the taxpayer transfers the property and it does not qualify as a principal residence.

The long-term implications for all involved should inform each transfer property decision.

The principal residence exemption can eliminate that tax, but only if the property qualifies. A cottage, rental property, or second home usually does not.

The owner may have used a property as a principal residence for only a portion of their ownership period. That can reduce the taxable portion of the gain, but it does not eliminate it entirely. Timing also matters. Triggering tax during your lifetime versus at death can lead to very different outcomes depending on income, other assets, and overall estate planning.

Probate applies when property passes through an estate. In Ontario, the Government of Ontario sets this at roughly 1.5 percent of the estate value over $50,000. On an $800,000 property, that is about $12,000. It is a cost, but often smaller than the tax consequences people are trying to avoid.

Probate can complicate the process when you transfer property, but careful planning can mitigate these issues.

Many overlook the land transfer tax, which can still apply even between family members if the transfer involves payments or mortgages, so readers recognize all costs.

Focus on these key areas to make practical property transfer decisions, as grasping capital gains tax, probate, and land transfer tax is essential.

Gifting property

Gifting is often the first idea people consider. Transfer the property now, avoid probate later, and keep things simple.

Families often look to transfer property to simplify their affairs, but they need to understand the implications fully.

From a legal standpoint, it is straightforward. A lawyer transfers title, and ownership changes.

From a tax standpoint, the tax authorities treat it as a sale at fair market value.

The property not being your principal residence results in an immediate capital gains tax liability. Families often encounter difficulties here, particularly concerning cottages.

A cottage purchased decades ago for a modest amount may now have a significant increase in value. Without prior planning, the transfer could cause significant tax liability that year. Payment of the bill is required, regardless of any funds that may arrive.

Understanding how to transfer property can prevent unexpected tax bills and other complications.

After a property transfer, control shifts, which can make you feel more secure or uncertain. Considering this helps you make empowered choices about your family’s future.

A situation that comes up from time to time is where a parent transfers a home to a child, and later the child goes through a separation or financial difficulty. The property is now exposed in a way that was never intended.

Gifting can work well, especially for principal residences, but consulting a professional ensures you feel reassured and avoid costly mistakes related to timing and control.

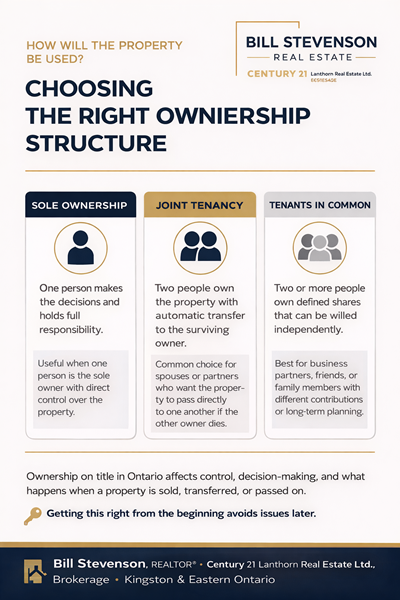

Adding someone to the title

It’s common to add a family member to a title, but people often misunderstand how it works.

Adding someone to the title is a way to transfer property, but it can lead to shared ownership risks.

The usual goal is to avoid probate. When one owner passes away, the property transfers automatically to the surviving owner.

This component is operational.

The issue arises when one includes the name.

When you choose to transfer property, clarity about ownership is vital.

Often, people consider adding someone to the title a gift of a portion of the property. Transferring half the property may cause half the gain to be recognized then, which is referred to as a partial disposition.

A common example is a parent adding an adult child to the title on a home that has increased significantly in value. The intention is to simplify the estate. Instead, it triggers part of the capital gain immediately, complicating the ownership structure.

The result is often unexpected. The property now has shared ownership, and part of the capital gain may trigger immediately. If there are other children, the arrangement can also create questions about fairness later on. What started as a simple step to avoid probate can turn into both a tax issue and a family issue.

The decision to transfer property impacts not only financial outcomes but also family dynamics.

Control also changes. Decisions about refinancing, selling, or even maintaining the property now involve more than one owner. The property may also become exposed to the other person’s legal or financial situation.

This approach can be useful sometimes, but it is not a simple administrative step. It changes both the tax and ownership meaningfully.

Selling to family

Selling the property to a family member is often a more structured approach.

It creates a straightforward transaction, with defined terms and expectations. It avoids some of the ambiguity that comes with gifting or partial transfers.

Tax authorities still consider the transaction to be at fair market value, even if the sale price is lower than the market value. That part does not change.

When selling to family, it is crucial to document the transaction clearly to avoid misunderstandings when you transfer property.

Where this approach is useful is in its structure.

Sometimes, families use a Vendor Take-Back mortgage. The seller is providing financing for a portion of the sale, enabling the buyer to pay in installments. A child could gain property without immediate full traditional financing.

👉 See our full guide on Vendor Take-Back Mortgages

For example, a parent may sell a home valued at $700,000 and agree to finance a portion of that price. The child makes payments under agreed terms and properly documents the transaction from the beginning.

Such arrangements can help families to transfer property smoothly while ensuring everyone understands their responsibilities.

While preserving the sales structure, this approach allows flexibility in payment arrangements. It can also help avoid informal arrangements that often lead to misunderstandings later.

Sometimes, families agree on informal terms without documenting the arrangement clearly. That can work for a period, but problems arise when circumstances change. A sale, refinance, or disagreement about payments can reveal what was not originally agreed upon.

Structuring the transaction properly from the beginning helps avoid those issues. Logical terms around price, repayment, and expectations reduce the risk of conflict later. It also ensures that both sides understand how the arrangement fits within broader tax and ownership considerations.

Taking the time to plan how to transfer property is vital for avoiding conflicts later.

There is also a timing element. A structured sale can allow for better coordination with other financial decisions, including retirement planning or future transfers. Without that structure, families may react to situations rather than planning for them.

Transferring through a will

One of the most trusted ways to transfer property is through a will.

Ownership stays with you during your lifetime. The property passes through your estate under your instructions.

Probate applies, and the cost is predictable.

This option allows families to transfer property in a structured manner, reducing the risk of complications.

This approach avoids changes to ownership while you are alive. It also reduces the risk of unintended consequences, such as tax being triggered earlier than expected or ownership becoming complicated.

There is also a timing advantage. At death, capital gains activate and enable enhanced integration with the estate’s components. Sometimes, that timing can be beneficial.

For families with multiple beneficiaries or more complex situations, this approach often provides the clearest path forward.

The process changes substantially if the property does not transfer in advance but passes through an estate. See our guide on Selling an estate property in Ontario for a full breakdown of probate, executor responsibilities, and timelines.

Using a Trust

A trust can be an effective way to maintain control when you want to transfer property.

Individuals use trusts when they focus on control and long-term planning.

A structure, rather than direct ownership transfer, governs the property’s management and determines its beneficiaries.

For blended families and those worried about future property handling, a trust can be advantageous. It allows decisions to be structured in advance rather than left to circumstances later.

The trade-off is complexity. A trust requires legal setup, ongoing administration, and careful tax planning. If you do not handle the plan correctly, tax liabilities may arise because taxing authorities could treat the property as sold over time, even though no actual sale occurs.

Those seeking to transfer property should consult with experts who understand these complexities.

Professionals should guide the structure of a trust from the start, as it functions as a long-term planning tool.

Situations that shape the decision

Real-life situations drive these decisions more than theory.

Parents helping children buy is one of the most common. They may co-sign a mortgage, go on title, or provide financing. Each option presents different tax and ownership implications, particularly when someone eventually sells the property.

Cottages require careful attention. Many owners have held their cottages for years, realizing significant unrealized gains. They also involve multiple family members, which adds another layer of complexity.

Family cottages often create the most complicated transfer decisions. Siblings often share cottages, or families pass them down through generations. This sharing and passing down creates financial and practical challenges.

Ownership is only part of the issue. Unclear expectations can lead to tension over maintenance costs, usage, upgrades, and long-term responsibility. What begins as a shared asset tied to family history can quickly become difficult to manage without structure.

A formal agreement for shared ownership or a well-defined exit plan is frequently as vital as the transfer itself.

Many families delay decisions because the property carries emotional value and financial value. Over time, that delay can increase the tax exposure as the property continues to appreciate. When families finally address the issue, they often have more limited options, and sometimes they must sell the property simply to cover the tax.

The financial realities and the practical realities often coincide, so you should start cottage succession planning well before you expect a transfer.

A different scenario occurs when a parent lives in a property that their adult child owns. That ownership structure removes the parent’s ability to claim the principal residence exemption. Selling the property could cause the child to bear the entire capital gain. Over time, that gain can become significant, especially if the property continues to increase in value. The arrangement may have made sense at the beginning, but without planning, the long-term tax outcome is often worse than expected.

Transfers between spouses or common-law partners

Spousal transfers can simplify how to transfer property, but understanding the tax implications is critical.

The tax treatment for transfers between spouses or common-law partners differs from other family transfers. Many times, you can transfer the property without immediately triggering capital gains tax, because you transfer it at its existing tax value rather than current market value.

This does not mean people avoid tax. Usually, the government defers it. When the property eventually sells, someone still recognizes the gain, and sometimes the original owner may still report it.

Structuring a transfer at market value is another option; this approach can trigger taxes sooner but streamlines ownership later. These decisions depend on the broader financial and estate plan.

The Canada Revenue Agency outlines these rules, particularly for transfers between spouses and related trusts. Because of the attribution rules and potential elections involved, this is an area where professional advice is important before deciding.

When plans change

Being proactive about how to transfer property can ease issues during significant life changes.

Common-law relationships also require attention. Ownership does not automatically follow the same rules as marriage. Title and agreements need to reflect the reality of the relationship.

No one expects all ownership changes.

Separation, divorce, or financial changes can force property decisions.

The organization of the property is vital when those situations arise. Ownership, tax implications, and financing all come into play simultaneously.

👉 Read: Spousal Buyout and Home Ownership After Separation

Planning does not prevent these situations, but it makes them easier to manage if they occur.

Common mistakes

The same issues repeat.

Education on how to transfer property can prevent common mistakes that families make.

People assume gifting avoids tax. It does not. People consider adding someone to the title simple. That is incorrect. People often think probate is the highest cost, but tax liabilities are usually more significant.

Another mistake is waiting too long. Delaying decisions can reduce flexibility and limit options.

Most issues arise not from the strategy itself, but from a misunderstanding of its operation.

Final thoughts

There is no single best way to transfer property.

Thinking through the options available to transfer property will lead to better family outcomes.

Each option involves trade-offs between tax, control, and risk. The right decision depends on the property, the family situation, and long-term plans.

Understanding the full picture before making a move prevents costly mistakes.

Professional advice

Property transfers involve legal, tax, and real estate considerations that need to work together. A decision made in isolation can create problems in another area.

A real estate lawyer, an accountant, and a REALTOR® each bring a different perspective. Coordinating that advice helps ensure the structure fits the situation.

For legal guidance, firms such as Cunningham Swan LLP or Viner-Kennedy LLP assist with property transfers and estate planning matters.

Coordinating advice can significantly impact how to transfer property effectively.

Frequently asked questions

Can I transfer my house to my child without paying capital gains tax in Ontario?

Most times, no. Most times, no. People consider the transfer a sale at fair market value, meaning taxes might apply if the property doesn’t qualify as a principal residence.

Does adding someone to the title avoid probate?

It can, but it may trigger capital gains and create shared ownership risks.

These insights can empower families to transfer property confidently.

Is gifting better than selling?

Not from a tax standpoint. The tax standpoint treats both similarly. Selling provides more structure and clarity.

Do I still pay land transfer tax?

Certainly, but it depends on the circumstances. Key factors include the structure of the transfer and the consideration.

What is the safest approach?

Often transferring through a will. Other strategies require careful planning to avoid unintended consequences.

Understanding the best strategies to transfer property can help mitigate risks.

Don’t miss these guides.

Understanding how property transfers work in Ontario is only part of the picture. These guides expand on buying, selling, and ownership decisions, helping you structure a transfer properly and avoid costly mistakes before moving forward.

Kingston and Area Home Buyers Guidebook 2026

It gives a comprehensive overview of the buying process, detailing the initial ownership structure and how early decisions impact future transfers.

Explains how property value, timing, and preparation influence financial outcomes, which becomes critical when deciding whether to sell, gift, or transfer.

Working with a Kingston REALTOR®

Support from family can play a crucial role when you wish to transfer property.

Shows how local expertise helps identify risks in ownership changes, especially in family transfers or non-standard transactions.

First Home Purchase: Kingston Area

Helps frame how first-time buyers often rely on family support, and how those prior arrangements can impact future ownership and tax exposure.

House Hunting Online: What Buyers Need to Know

Describes how buyers evaluate properties today, which matters when someone eventually sells or re-enters a transferred home into the market.

Keeping these factors in mind will help individuals better navigate how to transfer property.

Call to action

If you are thinking about transferring property to family, take the time to get it right.

Making an informed decision about how to transfer property will ultimately benefit your family.

A decision made quickly can create tax or legal issues that last for years.