A solid budget protects you from surprises and gives you confidence when the right home appears. The goal is not to spend the most you can, but to choose a home that fits your life today and still works a few years from now.

In Kingston and the surrounding area, your home purchase goes beyond price. Property taxes, utilities, maintenance, and future changes in income all affect what you can comfortably afford. Before you start your search, it is worth taking the time to understand your actual monthly costs and where you want your finances to be.

The right home is not just one you can buy. It is one you can comfortably live in.

Focus first on lender scrutiny.

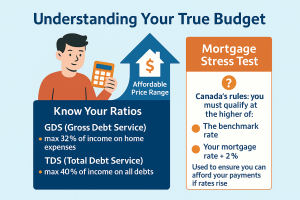

Before you tour homes, it helps to understand how lenders decide what you can afford. They use two key ratios, Gross Debt Service and Total Debt Service, to measure how much of your income can go toward housing and overall debt.

In simple terms, these guidelines set the upper limit of what a lender may approve. They are not a target you need to reach.

Canada’s mortgage stress test also plays a role. You must qualify at a higher interest rate than your actual mortgage rate, which can reduce your maximum purchase price. The goal is to make sure you can still carry the home if rates rise.

Knowing your GDS, TDS, and stress test limits before you fall in love with a property keeps your finances on solid ground. It allows you to focus on homes that fit your situation, not just what a lender will offer.

A brief conversation with a mortgage professional, or even a reliable online affordability calculator, will give you a clear working range. From there, you can build a plan that reflects your income, your lifestyle, and where you want to be in the next few years.

Understanding these numbers early helps you avoid financial strain later and keeps your home search grounded in what truly works for you.

💡 Pro Tip: Use the CMHC mortgage affordability calculator to get a realistic view before meeting with your bank or mortgage broker.

Plan for the next three to five years.

Affordability is not just about what works today. It is about how your life may change over the next few years.

Income can shift. Work situations change. Family plans develop. Even steady households deal with unexpected costs, from car repairs to higher insurance or utility bills. These are not rare events; they are part of normal life.

When you are choosing a home, it helps to leave room for those changes. A property that fits comfortably within your budget today will be much easier to manage if something shifts tomorrow.

Many buyers run into trouble by stretching to the top of their range, assuming everything will stay the same. When it does not, the home feels like a financial strain instead of a place to enjoy.

A more effective strategy involves reserving funds in your budget. Having this flexibility means you have alternatives, whether for overcoming obstacles, implementing upgrades, or just living comfortably without the burden of constant financial worry.

Understand the actual monthly costs

The purchase price is only part of the picture. What matters just as much is what it costs to live in the home each month.

In Kingston and area, that includes property taxes, utilities, insurance, and ongoing maintenance. Property type, age, and location influence these costs, which can accumulate rapidly if not addressed proactively.

A newer home may have higher taxes but lower maintenance. An older home may come with a lower purchase price, but higher repair costs. Rural properties can introduce additional considerations such as well and septic maintenance, while some neighbourhoods may have higher insurance costs.

Looking at the full monthly picture helps you avoid surprises. It also makes it easier to compare different homes realistically, rather than focusing only on the purchase price.

A home that fits comfortably within your monthly budget is far more sustainable than one that stretches your finances, even if the purchase price seems manageable at first.

Look for Long Term Value

It is easy to get drawn in by finishes and décor, but long-term value comes from the fundamentals.

Neighbourhoods with steady demand, practical layouts, and properties that can adapt over time hold their value more consistently. Homes near schools, parks, transit, and everyday services are usually easier to live in and easier to sell when the time comes.

A flexible layout matters as well. A home that works for different stages of life gives you more options, whether your needs change or the market shifts.

Your budget still sets the boundaries. The goal is to find the best combination of location, layout, and condition within a price range that remains comfortable.

A well-located, adaptable home is more likely to protect your investment and give you stability.

Where your budget goes further

In Kingston and the surrounding area, how far your budget goes depends heavily on location.

Neighbourhoods like Kingscourt often provide more accessible entry points, with smaller detached homes and duplexes close to downtown and major routes. These areas appeal to buyers who want to stay central without stretching their budget.

Rideau Heights is another area buyers are watching more closely. With ongoing redevelopment and improvements, it offers lower entry prices and the potential for long-term growth as the neighbourhood continues to change.

Looking beyond the city, communities such as Loyalist, Verona, Harrowsmith, and Napanee can offer more space for the price. Larger lots and quieter surroundings appeal to buyers who are open to a different pace, even with the tradeoff of a longer commute.

Each option comes with a unique balance of cost, location, and lifestyle. Comparing them within your full budget helps you choose a home that works both financially and day to day.

Bringing it all together

Matching your home to your budget comes down to more than a purchase price. It involves understanding what lenders will approve, what the home will cost each month, and how your situation may change.

In Kingston and the surrounding communities, buyers have more choice than they did just a few years ago. That creates opportunities, but it also makes it more important to stay focused on what works for your finances.

A home that fits comfortably within your budget gives you flexibility. It allows you to handle unexpected costs, adjust to changes, and enjoy the home without constant financial pressure.

Taking the time to plan before you buy leads to better decisions and a more sustainable investment.

________________________________________________________________________________________________________________________

Frequently asked questions

How much should I set aside for closing costs?

In Ontario, closing costs typically range from 2% to 4% of the purchase price. That includes land transfer tax, legal fees, adjustments, and insurance. First-time buyers may qualify for rebates that reduce the total.

Should I wait for interest rates to drop?

Trying to time the market is hard. Lower rates can help, but they often bring more competition. In a balanced market, buyers have more choice and room to negotiate. The better approach is to buy when the numbers work for your income and your lifestyle.

How do I know if a neighbourhood will hold its value?

Look for steady demand and strong fundamentals. Access to schools, parks, transit, and everyday services tends to support long-term value. Layout and usability of the home matter as well, often more than cosmetic finishes.

Are rural homes riskier to buy?

Rural homes can offer excellent value, but they require more due diligence. Wells, septic systems, heating, and access all vary by property. A proper inspection with someone familiar with rural homes is important before moving forward.

Is renting the smarter choice right now?

It depends on your timeline. Renting can make sense if you expect to move within a year or two. If you plan to stay for three to five years, owning may provide more stability and the chance to build equity. Cash flow matters as well. If buying stretches your budget too far, renting may be the better option for now.

Don’t Miss These Guides:

Understanding your budget is only part of buying a home. These guides cover inspections, neighbourhood choice, hidden costs, and the full buying process across Kingston and the surrounding Frontenac, Lennox, and Leeds area.

Neighbourhoods in Kingston and Area

An overview of Kingston and nearby communities, including lifestyle, commuting, amenities, and how location affects long-term value.

8 Hidden Costs of Buying a Home in Ontario

Explains closing costs such as land transfer tax, legal fees, insurance, and ongoing expenses so you can plan ahead..

Kingston Homes: Rent or Buy in 2026

A practical comparison of renting versus owning, including local trends, flexibility, and long-term financial considerations.

First Home Purchase: Kingston Area

A step-by-step guide covering mortgage preparation, deposits, conditions, inspections, and the path from offer to closing.

______________________________________________________________________________________________________________

🔗 Helpful Resources

-

Mortgage Affordability Calculator (Ratehub.ca)

Estimate how much home you can afford based on income, debt, and down payment. -

Home Buyers’ Plan (RRSP Withdrawal Info)

Learn how to withdraw up to $30,000 tax-free from your RRSP to use as a down payment and understand repayment timelines. -

Ontario Land Transfer Tax Calculator

Calculate land transfer tax costs and rebates for first-time home buyers in Ontario.H