Budgeting for the Hidden Costs of Buying a Home in Ontario

The hidden costs of buying a home in Kingston and the area can add thousands of dollars beyond your down payment and mortgage payment. Most people only think about the price before buying, at closing, and for a little while after, so they’re surprised by extra costs.

Buying a home is one of the largest financial decisions most people will ever make. Whether you are purchasing your first home, moving up to a larger property, downsizing, or relocating to the Kingston area, most buyers focus on two numbers: the purchase price and the monthly mortgage payment.

While both are important, they only tell part of the story.

Every real estate transaction comes with additional expenses that can significantly affect your budget. You will incur some costs before closing, pay some on closing day, and others will arise during the first few months of ownership. Buyers who do not plan for these expenses can find themselves financially stretched just when they should enjoy their new home.

Proper planning is essential for buyers to budget effectively and avoid surprises. Understanding these hidden costs early, including property taxes that vary by property type and location helps prevent financial stress during the home-buying process.

Whether you are buying a condominium in Kingston, a family home in Amherstview, a rural property in South Frontenac, or a waterfront home near Sydenham, Gananoque, or Rideau Lakes, understanding these hidden costs will help you make more informed decisions throughout the buying process.

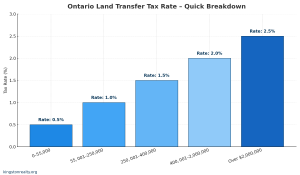

1. Land Transfer Tax: The Biggest Expense

For many local buyers, the land transfer tax is the single largest expense after the down payment.

People pay the land transfer tax once at closing, in contrast to property taxes, which are paid annually. The government bases the amount on the property’s purchase price and requires you to pay it before they transfer ownership.

Many buyers underestimate this cost simply because it is not part of the advertised purchase price. A buyer may carefully save for a down payment, only to discover they need several thousand dollars more to complete the transaction.

Fortunately, first-time homebuyers may qualify for a provincial rebate that can offset a portion of the tax. However, even with rebates for first-time buyers, all buyers should calculate their land transfer tax well before making an offer.

👉 Learn more about Land Transfer Tax rebates for first-time homebuyers on the Ontario government website.

The higher the purchase price, the larger the tax becomes. As home values have increased across Kingston and the area over the past several years, the land transfer tax has become an increasingly important part of the overall purchasing budget.

Buyers who understand their estimated land transfer tax and legal fees before they shop are less likely to encounter unpleasant surprises on closing day.

2.Legal fees, title insurance, and other closing expenses

Although legal fees are not hidden costs, an uninformed buyer might still end up paying more than they expected. Every real estate transaction requires legal representation.

Your lawyer performs a variety of important tasks, including reviewing documentation, conducting title searches, registering ownership, arranging mortgage registration, handling the transfer of funds, and ensuring completion of all agreement conditions.

Buyers usually set aside money for legal stuff, but don’t think about the extra fees on the last bill.

These expenses, commonly known as disbursements, may include registration fees, title searches, title insurance, courier costs, bank charges, and other administrative expenses incurred in completing the transaction.

Title insurance deserves special mention because many buyers are unfamiliar with it. The policy protects the homeowner and lender from specific title-related issues that might have gone unnoticed during the purchase process. Problems involving liens, survey discrepancies, fraud, or registration errors may all fall within the scope of coverage.

While none of these individual costs are typically overwhelming, together they can add substantially to the amount required on closing day.

Buyers should always ask their lawyer for an estimate early in the transaction to facilitate proactive planning and reduce last-minute surprises on closing day.

Learn more in our Home Buyer’s Guidebook

3. Home Inspection

A professional home inspection remains one of the smartest investments a buyer can make.

An experienced inspector can identify issues with roofing, structure, electrical systems, plumbing, insulation, moisture intrusion, heating equipment, windows, and other major components before buyers finalize the transaction.

However, many buyers discover they should look beyond a standard home inspection.

Properties throughout Frontenac, Lennox & Addington, and Leeds & Grenville, especially rural homes with private wells or septic systems, warrant further investigation to prevent costly surprises after closing.

Depending on the property, buyers may wish to consider well water testing, septic inspections, water quantity testing, WETT inspections for wood-burning equipment, surveys, zoning reviews, or waterfront-specific evaluations.

These additional reports add to the overall cost of purchasing a property, but they can also help buyers avoid far more expensive surprises after closing.

When viewed as part of the overall investment, inspections are often among the least expensive and most valuable costs associated with buying a home.

4. Statement of Adjustments: The Cost Most Buyers Never Expect

Few buyers understand the statement of adjustments until their lawyer explains it shortly before closing.

Basically, adjustments are just money back to the seller for stuff they already paid for after the deal was closed.

One of the most common examples involves property taxes. If the seller has paid taxes for a period extending beyond your possession date, you will reimburse them for your share of those prepaid taxes.

Condominium fees can create similar adjustments.

Rural properties often involve additional items. Closing commonly adjusts propane and fuel oil tanks, as well as other prepaid services.

Adjustments can lead to unexpected expenses for buyers unfamiliar with the process. A recently filled propane tank may contain hundreds or even thousands of dollars’ worth of fuel. While the buyer receives the benefit of that fuel, they also inherit the cost.

The adjustment is completely normal, but many buyers cannot budget for it because the early stages of the purchase process do not widely discuss it.

Understanding adjustments ahead of time allows buyers to keep additional funds available and avoid last-minute financial pressure.

Another of the hidden cost of buying a home in Ontario is appraisal fees. If you’re arranging a mortgage, your lender may require a professional appraisal to confirm the property’s market value. In Kingston and Eastern Ontario, appraisals typically cost $350 to $600, depending on the property’s size, type, and location.

The buyer usually pays this cost directly . While it primarily protects the lender by ensuring they don’t finance more than the home is worth, it also benefits you by providing an independent check that the purchase price is in line with market value.

5. Rental Equipment and Service Contracts

One of the most overlooked costs in Ontario real estate involves rental equipment.

Many buyers think that equipment attached to the home automatically belongs to the seller. That is not always the case.

Hot water tanks are perhaps the most common example, but they are far from the only ones. People may also rent furnaces, water softeners, reverse osmosis systems, propane tanks, security systems, and other equipment.

These agreements can range from very reasonable to surprisingly expensive.

Before purchasing a property, buyers should determine exactly which items are owned and which are rented. They should also understand the monthly cost, contract terms, buyout options, and any obligations that transfer with ownership.

A monthly rental fee may seem insignificant at first glance, but several contracts can quickly add up over the course of a year.

Reviewing rental agreements before closing helps buyers understand the true cost of ownership and prevents unpleasant surprises after moving in.

6. Moving Costs and Immediate Move-In Expenses

Buyers often get too focused on closing costs and overlook the costs that hit as soon as they get their keys.

Moving itself can be expensive. Professional movers, truck rentals, packing supplies, temporary storage, fuel, and utility transfers all contribute to the overall cost.

For larger households or long-distance relocations, moving expenses can easily reach several thousand dollars.

The spending often continues after the moving truck leaves.

Fresh paint, appliances, window coverings, lawn equipment, tools, furniture, shelving, storage systems, and minor repairs frequently become priorities during the first few weeks of ownership.

Even buyers purchasing well-maintained homes often discover a variety of minor projects they want to tackle immediately.

Online affordability calculators rarely include these costs, yet new homeowners often encounter them as common expenses.

Don’t forget to budget for moving expenses; it’ll smooth things out.

💡 Tip from experience:

From a personal standpoint, I’ve found Frank The Mover to be quite reasonable for local moves. That said, I always recommend getting at least three written quotes before choosing a mover. Be sure to check reviews, including the Better Business Bureau (BBB). Unfortunately, there are cases where disreputable movers load your belongings and then demand extra fees before releasing your property. Doing your homework upfront helps you avoid stress on moving day.

7. Rural and Waterfront Property Costs

One advantage of living in Kingston and the area is the incredible variety of properties available.

Buyers can choose from urban neighbourhoods, rural acreages, hobby farms, waterfront homes, cottages, and country estates. However, these properties often come with responsibilities that urban buyers may not have experienced before.

Private wells require testing and maintenance. Water treatment systems may include ultraviolet purification units, water softeners, sediment filters, or reverse osmosis systems.

Septic systems require regular pumping and ongoing care.

Properties heated by propane, oil, wood, pellet, geothermal, or heat pump systems each have unique operating and maintenance costs.

Waterfront properties may include docks, shoreline protection, intake systems, pumps, boathouses, and seasonal maintenance.

Some rural properties also include private roads or shared access agreements that can create ongoing costs.

None of these expenses should discourage buyers from pursuing a rural or waterfront lifestyle. Many owners find the benefits far outweigh the costs.

However, buyers should understand these responsibilities before purchasing so they can budget appropriately and enjoy their property without further unexpected costs.

8. Insurance, maintenance, and emergency repairs

Perhaps the most important hidden cost is the one nobody can predict.

Every home requires maintenance.

Roofs eventually wear out. Furnaces need repairs. Appliances fail. Sump pumps stop working. Garage door openers break. Well pumps wear out. Trees come down during storms.

The question is not whether maintenance will occur. The question is when.

Home insurance helps protect against certain risks, but insurance is not a substitute for routine maintenance or emergency savings.

Insurance costs can vary significantly depending on the age of the home, its location, construction type, heating system, and proximity to water. Waterfront properties, older homes, and some rural properties may require specialized coverage or higher premiums.

For this reason, many financial professionals recommend maintaining an emergency reserve fund after closing.

Buyers who exhaust every available dollar on their down payment and closing costs often struggle when the first unexpected repair arrives.

Maintaining a financial cushion provides peace of mind and allows homeowners to address problems before they become larger and more expensive.

Budgeting for the Hidden Costs of Buying a Home in Ontario

Budget 3–5% of your purchase price for closing costs. On a $500,000 home, that’s $15,000–$25,000 besides your down payment.

Understanding the full breakdown of closing costs in Ontario gives you an edge. When you know what to expect — from land transfer tax to legal fees, adjustments, and potential extras — you can move forward with confidence and focus on making your new house a home.

Final Thoughts

The true cost of buying a home extends well beyond the purchase price and mortgage payment.

Land transfer tax, legal fees, inspections, adjustments, rental equipment, moving expenses, rural property costs, insurance, and ongoing maintenance all play an important role in determining what a home actually costs to own.

The good news is that you can plan for these expenses.

Whether you are buying your first home or your fifth, understanding these hidden costs before you make an offer can help you budget more accurately, avoid surprises, and move into your new home with confidence.

A home purchase should be exciting, not stressful. The more you understand about the full cost of ownership, the better prepared you will be to make a smart real estate decision in Kingston and the surrounding communities. If you need a mortgage broker to discuss costs, Kingston Mortgage Solutions has the experience.

_______________________________________________________________________________________________________________________

❓

Frequently Asked Questions About the Hidden Costs of Buying a Home

How much should I budget beyond my down payment?

Most buyers should budget an additional 3% to 5% of the purchase price for closing costs and immediate ownership expenses. Land transfer tax, legal fees, inspections, title insurance, moving expenses, utility setup fees, and other costs can add thousands of dollars beyond the down payment.

What is a statement of adjustment?

The statement of adjustments includes reimbursements paid to the seller for expenses they have already incurred beyond the closing date. Common examples include property taxes, condominium fees, fuel oil, and propane. Buyers often find these costs surprising because sellers and real estate agents discuss them less frequently than land transfer tax or legal fees.

Do I have to assume a rented hot water tank?

Not necessarily. Some rental contracts transfer automatically to the new owner, while others may offer buyout options. In either case these could be unexpected costs to the property buyer. Buyers should review all rental agreements before closing and understand the monthly costs associated with any rented equipment.

Are rural properties more expensive to own?

They can be. Rural properties often include private wells, septic systems, propane heating, water treatment equipment, generators, or private road agreements. While many buyers appreciate the lifestyle benefits of rural living, it is important to understand the ongoing maintenance and operating costs before purchasing.

What hidden costs should waterfront buyers expect?

Waterfront properties may entail additional maintenance expenses, including dock repairs, shoreline protection, intake systems, pumps, water treatment equipment, and seasonal upkeep. Insurance costs may also differ from comparable non-waterfront properties.

Can I add closing costs to my mortgage?

Most of the time, buyers must pay closing costs from their own funds. Lenders require land transfer tax, legal fees, inspections, and other closing expenses to be paid separately from the mortgage financing.

Should I get a home inspection on a newer home?

Even newer homes can have defects or maintenance issues. A professional home inspection can identify concerns that may not be visible during a showing and can provide valuable information about the property’s condition and maintenance requirements so you avoid unexpected costs in your new home.

Should I keep money in reserve for unexpected costs after closing?

Yes. Unexpected repairs and maintenance costs are a normal part of homeownership. Maintaining an emergency fund can help cover expenses such as appliance repairs, heating system problems, well or septic issues, and other unforeseen costs without creating financial stress.

📚 Don’t Miss These Guides

Understanding the hidden costs of buying a home can help you avoid surprises, but successful homeownership involves much more than budgeting for closing expenses. These guides explore financing, inspections, property ownership, and practical considerations that every buyer should understand before making an offer.

First Home Purchase: Kingston Area

Buying your first home involves more than saving a down payment. Learn about mortgage pre-approval, closing costs, inspections, financing options, and common mistakes that can affect your budget long after moving day.

Match the Home You Buy to Your Budget

A mortgage approval does not always mean a home fits comfortably within your budget. Explore how property taxes, utilities, maintenance, insurance, and ongoing ownership expenses should factor into your purchasing decision.

Working With a Kingston REALTOR®

A local REALTOR® can help buyers understand market conditions, identify potential concerns, negotiate effectively, and avoid costly mistakes throughout the buying process.

Waterfront Property in Kingston Area: Cottages, Year-Round Homes, and Buyer Guidance

Waterfront properties often involve additional ownership costs that urban buyers may not encounter. Learn about docks, shoreline maintenance, water systems, septic considerations, insurance requirements, and other factors that can affect both your budget and long-term enjoyment of a waterfront property.

House Hunting Online: What Buyers Need to Know

Online listings provide a significant starting point, but they rarely tell the entire story. Discover how to evaluate listings more effectively, recognize potential concerns, and avoid overlooking important costs while searching for your next home.