You may find you need to boost your credit score to qualify for a mortgage. Many buyers assume their income alone determines whether they qualify for a mortgage, but lenders look at far more than earnings. Credit history, debt levels, payment habits, and financial stability all play an important role in mortgage approval and interest rates.

To successfully boost your credit, it is vital to monitor your credit report regularly to identify areas for improvement.

Over time, planning and consistent financial habits can often improve credit scores. Even modest improvements may increase borrowing options, reduce interest costs, or improve overall mortgage flexibility.

If you want to boost your credit, consider setting up automatic payments to ensure you pay your bills on time.

For some buyers, boosting a credit score means paying down balances and correcting reporting errors. For others, it may involve reducing debt, avoiding missed payments, or delaying major purchases before applying for financing. To effectively boost your credit, it’s essential to understand these factors.

Understanding how to boost your credit can lead to enhanced financial opportunities and a better quality of life.

Preparing early can boost your confidence and make a significant difference, especially in a market where monthly affordability already matters more than ever.In doing so, you can boost your credit and enhance your chances of mortgage approval.

Remember that to truly boost your credit, maintaining a low credit utilisation ratio is crucial.

Your credit score can affect mortgage options, interest rates, and how much flexibility you have when preparing to buy a home.

Why your credit score matters?

Your credit score matters more than many buyers realize because understanding its impact can help you feel more in control of your home-buying journey. A credit score is not simply a number attached to a loan application. It helps lenders evaluate financial reliability and borrowing risk. Two buyers with similar incomes can qualify for very different mortgage amounts depending on their credit history, monthly obligations, and debt management.

Being informed about how to boost your credit will empower you during the home-buying process.

Higher credit scores lead to more mortgage options and better interest rates. Lower scores may limit lender choices, increase borrowing costs, or require additional conditions such as larger down payments or co-signers.

Many buyers overlook the importance of strategies to boost their credit, which can affect their mortgage options.

In Canada, many lenders consider scores above 760 to be very strong. Buyers in the 680-759 range still typically have good mortgage options available. Below that level, financing can become more restrictive, especially if there are additional concerns such as high debt ratios, missed payments, collections, or an unstable employment history.Credit also affects more than just mortgage approval. Insurance applications, lines of credit, and even some rental situations may involve credit checks. A strong financial profile creates flexibility and reduces stress during the purchasing process.

It’s essential to know that various financial aspects contribute to boosting your credit score.

Buyers wanting a better understanding of how mortgage lenders evaluate credit can also review the CMHC credit report guide, which explains how credit history and reporting can affect mortgage financing in Canada.

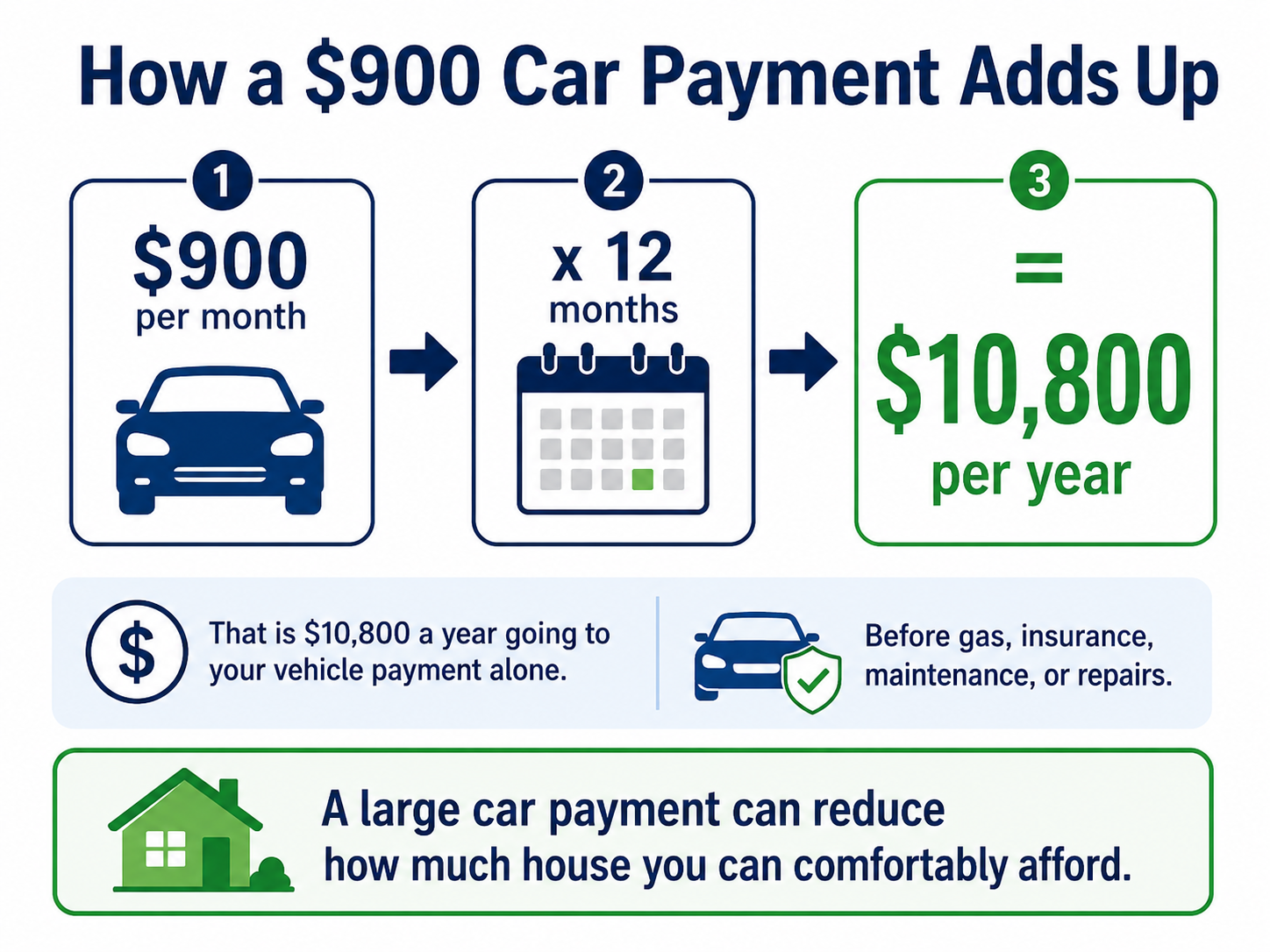

A large truck payment can affect how much house buyers can comfortably afford.

Viewing properties before consulting a mortgage expert.

Before making a purchase, consider how to boost your credit to improve your overall financial health.

Many first-time buyers browse listings online without speaking to a mortgage professional first. While searching homes can be exciting, it can also create unrealistic expectations if buyers do not yet understand what lenders may approve or what monthly ownership costs actually look like.Speaking with a mortgage broker or lender early provides a much clearer picture of affordability. Buyers gain a better understanding of what monthly payment range feels comfortable, how existing debt affects approval amounts, what down payment options may be available, what closing costs they should prepare for, and whether improving credit first could increase their purchasing power before entering the market.Or if we want stronger visual separation without bullets:

To boost your credit, ensure you are utilising credit responsibly and monitoring your accounts regularly.

Speaking with a mortgage broker or lender early provides a much clearer picture of affordability. Buyers must understand:

What monthly payment range feels comfortable?

Part of the plan to boost your credit includes understanding your spending habits and making adjustments.

How existing debt affects approval amounts.

What down payment options are available?

What closing costs should they prepare for?

Whether improving credit first could increase their purchasing power before entering the market.

The first version probably fits your blog style better because it flows more naturally and keeps the article conversational rather than instructional.

Car loans and monthly debt can quickly reduce buying power.

One of the most common issues affecting mortgage affordability today is vehicle financing. Modern car and truck payments have soared, and many buyers underestimate how heavily these monthly obligations affect debt ratios.

Buyers should also consult with professionals who can guide them on how to boost their credit effectively.

A large vehicle payment can reduce mortgage approval amounts by tens of thousands of dollars. Buyers sometimes focus only on household income while overlooking how lenders evaluate total monthly obligations.Before adding fuel, insurance, maintenance, or repairs, a large monthly car payment can reduce how much home a buyer can comfortably afford.Before accounting for fuel, insurance, upkeep, or fixes, a monthly car payment of $900 equates to over $10,000 each year.For rural buyers, vehicles are often a necessity rather than a luxury. Longer commutes, winter driving, and country properties frequently require reliable transportation. However, balancing vehicle costs alongside future homeownership is extremely important.Buyers preparing for a mortgage should avoid taking on new vehicle loans, furniture financing, or additional credit shortly before purchasing a home to help reduce financial stress and ensure smoother approval. By working to boost your credit score today, you’ll secure better loan deals and wider choices in the future.

Check Loans Canada for a bit more info on this subject.

Boost your credit score before your home search

Start early by taking action to boost your credit before you begin your home search.

Usually takes time rather than days or weeks to boost your credit score. By slightly improving your score, for instance, from 680 to 720, you can unlock more loan choices and pay less interest, making it easier to own a home.Reducing credit utilization is a highly effective tactic. Keeping balances near your credit limit negatively affects your score, even with on-time payments. Keeping balances lower relative to available limits helps.

Each effort you make to boost your credit can help you secure a more favourable mortgage deal.

Consistency also matters. Missed payments on credit cards, loans, or even mobile phone accounts can damage credit history. Setting up automatic payments or reminders may help avoid accidental late payments.

Buyers should also review their own credit reports before applying for financing. Errors occasionally occur, and correcting inaccurate information early can help avoid problems later during the mortgage process. The Financial Consumer Agency of Canada also provides practical guidance on improving credit habits and understanding how credit reporting works through its FCAC Canada credit score resources.

By informing yourself about how to boost your credit, you prepare yourself for a smoother purchasing process.

Opening several new accounts in a short period may also temporarily reduce scores. Buyers planning to enter the market within the next year are often better served by maintaining stability rather than applying for multiple new loans or financing plans.For buyers recovering from past financial difficulties, improvement is still possible. Rebuilding credit takes patience, but many buyers successfully move into homeownership after taking time to stabilize debt and rebuild payment history.

Preparing financially beyond the credit score itself

Strong credit alone does not automatically create comfortable homeownership. Buyers also need to prepare for the realities of ongoing ownership costs.Lenders review debt service ratios, employment stability, income consistency, savings history, and down payment funds. Buyers should also maintain emergency reserves, especially when purchasing older homes or rural properties, where unexpected repairs can be more expensive.In Kingston and the area, buyers considering older homes, waterfront properties, or country homes should carefully plan for maintenance costs, including wells, septic systems, propane heating, private roads, shoreline protection, and longer travel distances, which can all affect monthly budgets.

Finally, remember that a plan to boost your credit is an investment in your future homeownership journey.

A mortgage approval may show what a lender will finance, but buyers should also carefully consider what will allow them to live comfortably after moving in.

The strongest buyers are usually not the ones rushing into the market. They are the buyers who prepare early, understand their finances, improve their credit where needed, and speak with mortgage professionals before beginning serious home searches.That preparation creates confidence during negotiations, reduces surprises during financing, and often leads to better long-term financial decisions.Buying a home is one of the largest financial commitments most people will ever make. Strengthening credit, reducing debt, and understanding true affordability can make the entire process smoother and far less stressful.

Don’t Miss These Guides

Improving your credit score is only one part of preparing for homeownership. These additional guides explain how lenders evaluate buyers, how affordability works in today’s market, and what steps buyers should take before beginning their home search.

Explains how lenders evaluate credit profiles and why two buyers with similar incomes may qualify for very different mortgage amounts or interest rates.

outlines the differences between early lender estimates and a full mortgage review, helping buyers understand why proper pre-approval matters before making an offer.

Outlines many of the expenses buyers overlook, including closing costs, moving expenses, utility setup, insurance, maintenance, and unexpected repairs after possession.

Hi, let's connect on helping you with your property needs.

Bill Stevenson

I consent to receiving communications from Bill Stevenson, including calls, emails, and texts. To unsubscribe at any time, I can respond with 'stop' or use the unsubscribe link provided in the email messages.