Vendor take-back mortgages are reappearing in Kingston and the surrounding area as the market shifts into a position many buyers have been waiting for. There is more inventory, more time to decide, and more negotiating room. Prices have not fallen enough to fully restore affordability, and that tension is where many deals stall.

Buyers can see the opportunity, but financing doesn’t always align. Sellers still expect fair market value and are not eager to reduce the price to make a deal work.

One option that is reappearing in this type of market is the vendor take-back mortgage.

What is a vendor take-back mortgage? It’s a financing option in which the seller helps the buyer by providing part of the purchase funds, benefiting both parties by easing the transaction process and avoiding price reductions. A vendor take-back mortgage, often called a VTB, is when the seller agrees to finance part of the purchase price. Instead of relying entirely on a bank or traditional lender, the buyer arranges a first mortgage for a portion of the purchase, and the seller provides a second mortgage for the remaining amount.

The buyer then makes payments to both the institutional lender and the seller, according to the terms negotiated in the agreement.

Vendor take-back mortgages are not new, but they are becoming more relevant again as financing conditions tighten. For example, WOWA’s resources break down structuring how these arrangements in more detail. They also outline how vendor financing works in Canadian real estate transactions.

Why this matters in today’s market

The current Kingston and area market reflects a common pattern seen in transitional periods. Buyers are more cautious. Lenders are more restrictive. Monthly payments matter more than ever. Sellers often anchor themselves to recent sale prices and resist downward adjustments.

A vendor take-back mortgage can help bridge that gap without forcing either party into an uncomfortable position.

Instead of reducing the price, the seller can assist with financing. Instead of walking away, the buyer can move forward with a structure that makes the purchase manageable.

How it helps buyers

For buyers, the major benefit is access. For example, a VTB can help a buyer qualify for a property they might not otherwise afford by reducing the amount needed from a bank, making the purchase possible.

It can also reduce the immediate pressure of higher interest rates, depending on how the seller structures the loan. Sometimes, the seller may offer a short-term arrangement that allows the buyer to refinance later when conditions improve, helping buyers with high incomes but limited down payment flexibility, or those purchasing in higher price ranges where qualification thresholds are more restrictive.

A VTB can reduce the amount required from a traditional lender, which may allow a buyer to qualify for a property that would otherwise be just out of reach. Sometimes, the seller may offer interest-only payments for a period, which can reduce initial carrying costs, although the full balance will still need to be repaid later.

Lenders often treat vendor take-back mortgages as secondary financing, which can affect qualification and structure. Mortgage-focused resources such as True North Mortgage provide additional insight into how lenders view these arrangements.

How it helps sellers

For sellers, a vendor take-back mortgage can be a strategic move that enhances their control over the sale, making them feel more empowered to influence the outcome positively.

It can increase interest in the property by opening the door to more qualified buyers. It helps keep the asking price steady rather than relying solely on price cuts to stimulate interest. Interest payments over the term of the agreement also create a steady income stream.

In slower markets, that combination can make the difference between a listing that sits and one that sells.

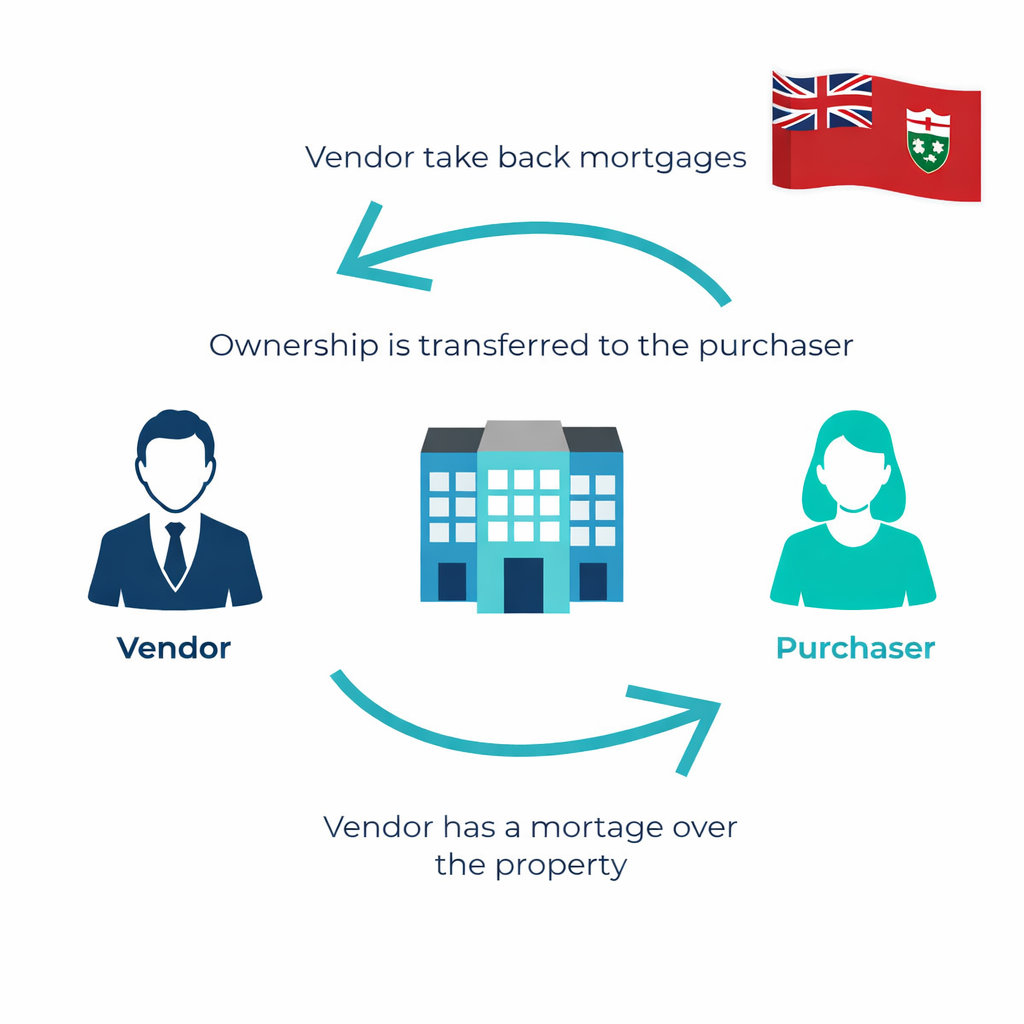

The diagram below shows how a typical vendor take-back mortgage works, including ownership transfer and the seller’s financing role.

The realities and risks

A vendor take-back mortgage involves risks, but understanding the importance of proper legal structure and clear expectations can help sellers and buyers feel reassured and confident in managing those risks effectively.

From the seller’s perspective, there is risk. You are effectively acting as a lender, which means you are relying on the buyer’s ability to make payments. Proper legal protection, including mortgage registration and clear default provisions, is essential.

From the buyer’s perspective, the obligation is real. Carrying two layers of financing requires discipline and planning. There should also be a coherent plan for how to end the arrangement, usually by getting new financing or paying off the loan when the time is up.

Legal and financial advisors deem it essential to proceed before the VTB’s position affects both risk and flexibility, especially if the VTB ranks below a first mortgage, meaning the primary lender gets paid first in a default, along with its terms.

Family members can also use vendor take-back mortgages in non-arm’s length transactions, like sales between them. While this can help a buyer move forward, it requires careful structuring, proper valuation, and clear legal advice to avoid unintended financial or tax consequences.

Where vendor take-back mortgages are most common

In Kingston and across Eastern Ontario, vendor take-back mortgages appear in specific situations.

They often appear in higher-priced homes where financing gaps are larger, or in rural areas with stricter lender criteria, such as properties that have been on the market for a long time, prompting sellers to consider alternative financing options.

Occasionally, people use them as a short-term solution when timing is an issue, which allows a buyer to secure a property now and restructure financing later.

Final thoughts

When buyers have many options but are price-constrained, vendor take-back mortgages provide a useful solution for closing sales.

They are not suitable for every transaction, but in the right situation, they can align the interests of both buyer and seller without forcing either side into a compromise that feels wrong.

When a deal is close to completing but not quite working, this is one tool that can bring it together.

Frequently Asked Questions

What is a typical structure for a vendor take-back mortgage?

Most vendor take-back mortgages function as a second mortgage behind a traditional lender. The buyer secures primary financing through a bank, and the seller provides additional financing for a defined portion of the purchase price. The terms usually include an agreed interest rate, a payment schedule, and a set maturity date when the lender requires repayment or refinancing of the balance.

Are vendor take-back mortgages common in Ontario?

They are not the norm in most transactions, but they are well-established and legally recognized in Ontario. Their use increases in markets where financing is tighter or where the gap between buyer affordability and seller expectations widens.

What interest rate do they typically charge?

Buyers and sellers negotiate the interest rate. It is often higher than a traditional mortgage rate to reflect the added risk to the seller. However, buyers and sellers can also structure it competitively, depending on the situation and their motivations.

How long does a vendor take-back mortgage last?

Most VTB agreements are brief, lasting 1-3 years, which gives the buyer a chance to boost their finances or wait for better market conditions before they can refinance and pay the seller.

What happens if the buyer cannot repay the loan

If the buyer defaults, the seller has legal remedies similar to those of any mortgage lender, including enforcement through a power of sale or other legal processes. Proper documentation and registration are essential to protect that position.

Can a vendor take-back mortgage prevent the need for a price cut?

Sometimes, yes. Instead of lowering the price, a seller can offer financing that makes the purchase more affordable, preserving the sale’s value while still allowing the buyer to move forward.

Don’t miss these guides

Understanding how vendor take-back mortgages work is only part of the picture. These guides expand on financing, negotiation, and market strategy, helping you decide when creative options like a VTB make sense and when a more traditional approach is the better path.

Kingston and Area Home Buyers Guidebook

A complete guide to buying, including funding, criteria, and closing. It clarifies the role of a vendor take-back mortgage in a conventional purchase.

Covers pricing, marketing, and negotiation strategies. Particularly relevant if you are considering offering a vendor take-back mortgage to attract buyers without reducing your price.

Working with a Kingston REALTOR®

It explains how parties manage deal structure, financing layers, and negotiations behind the scenes, particularly when vendor financing is involved.

First Home Purchase: Kingston Area

Focuses on affordability, qualifications, and realistic expectations. Useful for buyers exploring whether a vendor take-back mortgage could help bridge a financing gap.

House Hunting Online: What Buyers Need to Know

Shows how to evaluate listings properly and identify properties that may present financing challenges, where options like a vendor take-back mortgage are more likely to appear.