Many Kingston and area residents are weighing a significant financial decision: continue renting or move toward home ownership. Shifting mortgage rates, developing lending requirements, and steady rental demand have made the conversation more nuanced than it was even a few years ago. What once felt like a straightforward life step now requires careful evaluation.

In Kingston and the surrounding region, local factors influence the equation. Rental availability, property values, employment stability, and long-term growth patterns all shape the decision. For some households, renting offers flexibility and lower immediate responsibility. For others, buying represents stability, equity building, and control over future housing costs.

The right choice depends on more than monthly payments. It involves risk tolerance, time horizon, financial readiness, and personal lifestyle goals. In this article, we will examine the financial and practical considerations of renting versus buying in the Canadian context, so you can decide grounded in strategy rather than pressure.

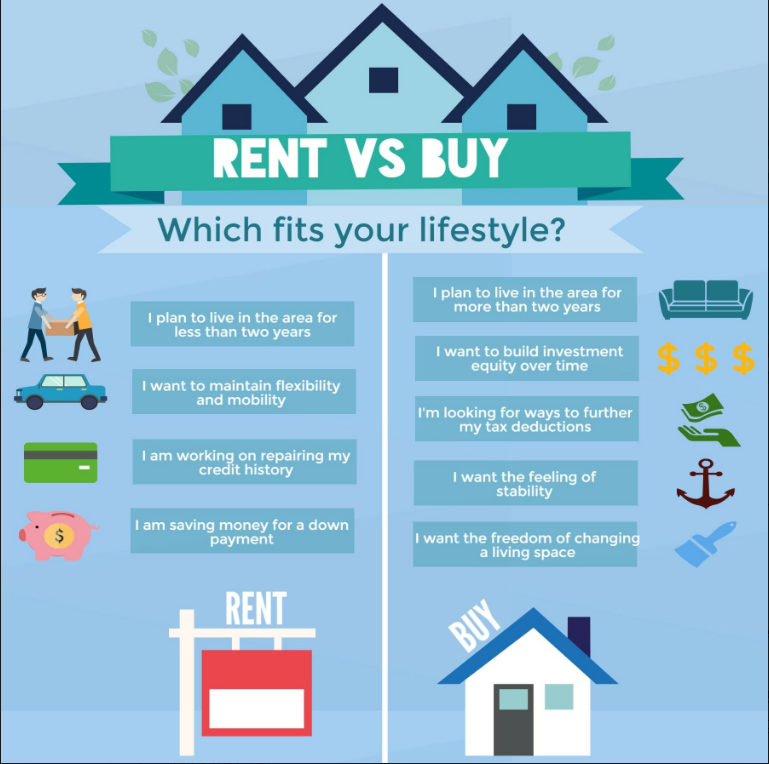

The Case for Renting

Renting often gets dismissed as “throwing money away,” but that’s not the complete story. Renting provides flexibility, especially for younger Canadians, newcomers, or those unsure about staying in one place long term.

Here are some key advantages:

-

Lower upfront costs. You don’t need tens of thousands for a down payment, closing costs, and moving expenses.

Consideration of Rent. It is advisable to consider renting, particularly when markets are unstable.

When deciding whether to lease or purchase, it’s essential to consider the current state of the rental market and how long you plan to rent.

-

Flexibility. Renting lets you move easily if your job changes, family needs shift, or you simply want a new neighbourhood.

-

Fewer maintenance surprises. Roof leaks, broken furnaces, or plumbing issues are the landlord’s problem, not yours.

-

Access to prime locations. In markets like Toronto or Vancouver, where buying may be out of reach, renting can still get you into the neighbourhood you want.

In high-demand areas, the choice to rent may offer access to properties that are otherwise unaffordable to purchase.

The downside, of course, is that your rent doesn’t build equity. Rents have also been climbing sharply across Canada, meaning the “savings” can disappear quickly. A Kingston two-bedroom that was $1,200 a few years ago can now easily be $1,900 or more.

The Case for Buying

Buying a home still carries strong financial and emotional benefits.

For many, the decision is a strategic move that reflects personal circumstances and market conditions.

Advantages include:

-

Building equity. Instead of paying money to your landlord, your mortgage payments build ownership in a property that may increase in value.

-

Stability. You’re not subject to annual increases or a landlord deciding to sell.

-

Personal freedom. Want to renovate the kitchen, add a garden, or finally get that dog? When you own it, the choice is yours.

-

Long-term wealth. Real estate has historically appreciated over the decades. In Ontario, even with recent price corrections, long-term owners have built significant equity.

The challenges of buying are real, too. Higher interest rates mean monthly payments are much steeper than even two years ago. First-time buyers may also struggle with saving a down payment, especially in competitive urban centres. In Kingston or Napanee, homes under $400,000 are rare, and many buyers are competing for the limited supply.

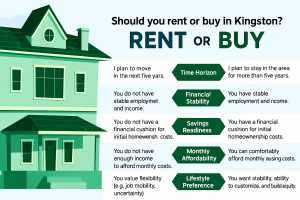

Running the Numbers

Deciding whether to rent or buy in 2025 comes down to your personal finances and goals. A helpful way to compare is to use a rent-vs.-buy calculator.

This tool lets you plug in your rent, local home prices, down payment, and mortgage rates to see how the costs stack up. In many Canadian cities, buying may only start to “beat” renting after 5–10 years of ownership. For temporary stays, renting often makes more sense. For those planning to put down roots, buying comes out ahead in the long run.

Lifestyle and Personal Goals

Numbers matter, but lifestyle counts too. Do you value freedom and flexibility, or do you crave stability and the pride of ownership? Are you comfortable handling repairs and yard work, or do you prefer calling the landlord when something breaks?

For some, renting is the right fit for a season of life, while for others, buying is part of a longer-term wealth-building strategy.

________________________________________________________________________________________________________________________

Looking Ahead: How “Future You” Might Feel

Sometimes the best way to decide today is to imagine how you’ll feel looking back years from now.

-

Relieved → In 20 years, you’ll likely be grateful you locked in ownership when you did, especially as rents continue to rise in Kingston.

-

Nostalgic → Even if your first home isn’t perfect, it might become the place where memories form, and you’ll cherish those moments when you look back.

-

Pride→ Buying a home is rarely easy, but decades from now, you may see it as one of your biggest life accomplishments.

-

Wishful → You might even wish you had stretched for a second property as an investment, given Kingston’s steady growth and rental demand.

Buying a home isn’t just about the numbers today. It’s also about the peace of mind, pride, and sense of stability that “future you” may thank you for.

The main point

There isn’t a one-size-fits-all answer to the rent vs. buy question. Your income, savings, career plans, and even your personality all play a role.

If you’re wrestling with the decision, talking to a REALTOR® who knows the Kingston and area market can make things clearer. I help clients every day who are weighing these choices, whether they’re saving for a first home, downsizing, or moving into a new neighbourhood.

Let’s sit down, review your options, and make sure your next move,whether renting or buying, fits your goals and your pocketbook.

📚 Don’t Miss These Guides

If you are weighing the decision between buying or renting in Kingston and the surrounding communities of Frontenac, Lennox & Addington, and Leeds & Grenville, these guides will help you understand affordability, costs, and market conditions before deciding.

Match the Home You Buy to Your Budget: What Kingston Buyers Need to Know 2025

Buying confidently starts with understanding what you can comfortably afford. This guide reviews mortgage qualification, debt ratios, budgeting, and practical financial planning tailored to Kingston and area buyers.

8 Hidden Costs of Buying a Home

The purchase price is only part of the equation. Learn about land transfer tax, inspections, legal fees, insurance, adjustments, and early maintenance expenses so you can budget accurately and avoid financial surprises.

First Home Purchase: Kingston Area

For many buyers, the rent-versus-buy decision comes down to timing and financial readiness. This guide explains the full home buying process, from mortgage pre-approval to closing, helping new buyers understand when they may be ready to enter the Kingston market.

Buyer’s vs. Seller’s vs. Balanced Markets

Market conditions influence whether renting or buying makes sense. This guide explains how different market types affect pricing, competition, and long-term strategy in Kingston and the surrounding area.

Considering a rent-to-own purchase

Some buyers consider rent-to-own as a path toward ownership when they are not yet ready for a mortgage. This guide explains how rent-to-own agreements work, the potential risks, and what buyers in Ontario should understand before signing a contract.