What Kingston area homeowners need to know

Reverse mortgages are becoming more visible throughout Kingston and the surrounding communities. Increasing home values have significantly boosted seniors’ equity, but they are facing financial pressure from the rising cost of living. While a reverse mortgage seems simple for a senior, it can trap them if they don’t grasp all the ongoing costs.

Many homeowners do not realize how quickly interest compounds, causing the debt to grow faster than expected and significantly draining their home equity. Understanding this helps you see the actual long-term costs and avoid surprises.

What a reverse mortgage is

A reverse mortgage is a loan secured against your home and available to Canadians aged 55 or older. You continue to own the home and live in it, but you do not make monthly payments. The balance increases with added interest each month. Repayment of the loan is required when you sell the home, move permanently, or pass away.

Most lenders allow access to a portion of your equity, often up to about 55 percent of the home’s value.

How it works

Approval is based on your age, the market value of your property, where the home is located, and the current interest rate environment. Older borrowers qualify for higher amounts because lenders expect shorter borrowing periods.

You have the option to take the funds all at once or to draw them as a monthly income. Since there are no required payments, the interest compounds, which means the balance grows a little faster every month. The home’s current market value, rather than its value on the day you signed, will dictate the repayment amount when it’s finally triggered.

One protection is the no-negative-equity guarantee. If the home’s value drops and the loan exceeds the sale price, the lender absorbs the difference. Your family is not responsible for the shortfall.

The good parts

The primary draw for many older adults is the option to stay in their residences and secure non-taxable funds. This money won’t change your OAS or GIS benefits and can cover medical needs, mobility improvements, heating system upgrades, or debt.

Reverse mortgages do not require income or credit approval, which helps seniors who no longer qualify for traditional products. They do not require monthly payments either, which can make day-to-day living easier for homeowners on a fixed income.

The reverse mortgage trap

The problem is that most borrowers underestimate how quickly interest grows when no payments are being made. After several years, the loan can take a larger share of the home’s equity than expected. Lenders also impose steep penalties for early repayment, and registering a reverse mortgage on title restricts other financing options.

The situation becomes even riskier when property taxes, home insurance, or maintenance fall behind. Failure to uphold any of these duties could cause the reverse mortgage lender to demand full repayment.

Independent legal advice safeguards seniors’ interests, empowering them to move forward with confidence.

The costly side

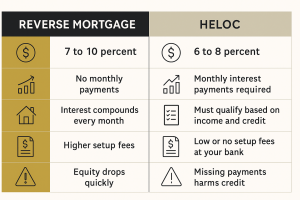

Reverse mortgages carry higher interest rates than mortgages, refinances, or HELOCs. In Canada, the rates typically range from 7 to 10 percent. Appraisal, administrative, and legal fees also apply, and penalties exist if you pay off the loan early.

The balance grows every month because interest compounds. The longer the loan remains active, the faster the balance increases, which can significantly reduce the inheritance left to your children or your estate.

Interest rates compared with HELOCs

The closest comparison for most homeowners is a HELOC (Home Equity Line of Credit). Most banks that you already work with will typically offer HELOCs. They require income and credit qualification, but the rates are typically far lower, often at prime plus a small percentage. In late 2025, that usually means between 6 and 8 percent.

The cost difference over several years can be substantial. HELOCs require monthly interest payments, whereas reverse mortgages do not, which is why their rates and fees are higher.

Scams and risks in Kingston and surrounding communities

The rise in reverse mortgages has led to an increase in scams. Some scams involve fake lender letters or fraudulent refinancing documents. Others hide behind online calculators designed to gather personal information. Be wary of contractors who push seniors toward reverse mortgages for renovations; it’s a major red flag.

Pressure from acquaintances, caregivers, or distant relatives is another concern. Independent legal advice is essential, and so is taking time to understand every term.

Misleading sales calls also occur. Some representatives gloss over penalties or long-term costs and focus only on the immediate cash. Always ask for written details and bring a trusted family member to meetings.

When a reverse mortgage may help

A reverse mortgage can make sense when a homeowner wants to remain in their home long term, does not qualify for a HELOC, and needs reliable access to funds for health care, accessibility, or significant repairs. It can also help homeowners who have no heirs or whose heirs are unwilling to use the home’s equity now.

When a reverse mortgage can cause problems

It is rarely a good idea for anyone planning to move, downsize, or sell within a few years, or for anyone whose home needs significant repairs. If you’re concerned about keeping up with taxes or insurance, or want to leave an inheritance, a reverse mortgage may not be the best choice. Recognizing these signs helps you make safer decisions.

How to protect yourself or your parents

Entering a reverse mortgage should always involve a review with an independent lawyer and a comparison of all options, including HELOCs, refinancing, downsizing, or provincial support programs. By reviewing the options, you can choose the most suitable and cost-effective solution for your situation.

Even making occasional voluntary payments can slow the long-term interest growth and preserve more equity.

Frequently asked questions

Is a reverse mortgage a good idea?

It depends on income, long-term plans, and the ability to maintain the home. It can help with cash flow, but the long-term cost is high.

What happens if I fall behind on property taxes or insurance?

The lender may demand full repayment, and this poses one of the most serious risks that requires consideration before signing.

Which value do they use when the loan ends?

At repayment or sale, the current market value applies, not the value from the day of original paperwork completion.

How much can I borrow?

Often up to about 55 percent of the home’s value.

What does HELOC mean?

HELOC stands for Home Equity Line of Credit. It is a revolving line of credit secured by your home.

Is a HELOC usually through the banks?

Yes. Your personal bank or credit union is most often the one that issues HELOCs.

Why choose a HELOC instead?

Lower interest rates, lower fees, and more flexibility. They are the better choice when income and credit allow.

Can I make payments on a reverse mortgage?

Yes, they permit voluntary payments, and these payments slow the growth rate of the balance.

What happens when I pass away?

Your estate must repay the balance, usually by selling the home.

📚 Don’t Miss These Guides

Housing decisions often involve financial planning, timing, and long-term lifestyle considerations. These related guides explore selling strategy, relocation planning, property condition, and practical preparation steps across Kingston and the surrounding Frontenac, Lennox, and Leeds communities.

Selling a long-held family property often involves more than just market timing. This guide explores planning, emotional considerations, and practical steps homeowners face when preparing a home for sale.

Relocating to Kingston and Area 2026

Moving to a new community involves understanding neighbourhood options, housing types, and lifestyle factors. This guide explains what buyers relocating to Kingston and the nearby Frontenac, Lennox, and Leeds counties should consider before making a move.

Home Inspections: Benefits for Buyers and Sellers

Property condition can influence negotiations and financing approval. This guide explains what inspections typically reveal and how both buyers and sellers use inspection results to better understand a home’s condition.

Top 10 Kingston Home-Selling Tips for 2026

Preparing a home for sale involves more than simply listing the property. This guide outlines practical strategies that help sellers present their home effectively and attract serious buyers throughout the Kingston area and neighbouring Frontenac, Lennox, and Leeds regions.