Land transfer tax is one of the most significant closing costs for Ontario homebuyers and investors. This cost is separate from the listed price and is determined at the point of property transfer. This guide details the tax’s operation, typical buyer costs in Kingston and Eastern Ontario, its application to various property types (condos, commercial buildings, vacant land), and first-time buyer rebates. A provincial estimator link is available for straightforward calculations. Understanding these differences helps buyers budget accurately for their specific property type.

What is a land transfer tax?

The province charges land transfer tax when ownership of a property transfers from one owner to another. Buyers pay this tax at closing. The tax applies to most real estate transactions in Ontario, including freehold homes, condos, commercial property, and vacant land.

The tax is determined by a tiered formula. We divide the purchase price into segments, and each segment has its own tax rate.

Toronto is the only municipality in Ontario that charges an additional municipal land transfer tax. Buyers in Kingston, Amherstview, Bath, Gananoque, and surrounding areas pay only the provincial tax.

Ontario land transfer tax rates

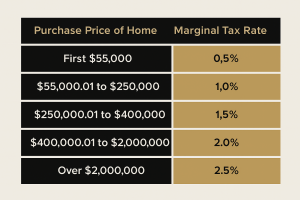

Ontario uses the following tax bracket structure:

0.5 percent on the first $55,000

1 percent on the portion from $55,000 to $250,000

1.5 percent on the portion from $250,000 to $400,000

2 percent on the portion above $400,000

2.5 percent on amounts above $2,000,000, where the property contains one or two single-family residences

The complete provincial formula is available here:

https://www.ontario.ca/document/land-transfer-tax/calculating-land-transfer-tax

Land transfer tax and commercial property

Commercial real estate purchases in Ontario are also subject to land transfer tax. The structure is almost identical to residential LTT, with one crucial difference.

Commercial, industrial, and multi-residential buildings do not fall under the 2.5% rate, which applies only to one or two single-family residences priced above $2 million.

A simple chart below illustrates the calculation of commercial LTT.

Ontario Commercial Land Transfer Tax Rates

Portion of Purchase Price Commercial LTT Rate

First $55,000 0.5 percent

$55,000 to $250,000 1 percent

$250,000 to $400,000 1.5 percent

Over $400,000 2 percent

These rates apply to:

Retail buildings

Office buildings

Industrial units

Apartment buildings

Mixed-use properties

Airbnb operates its buildings as commercial entities.

Commercial vacant land

Buyers of commercial and vacant land should understand that no rebates apply, so planning for the full land transfer tax is essential for budgeting and peace of mind.

Condos and land transfer tax

Land transfer tax applies to condo purchases even though you are not buying land in the traditional sense. The law still considers a condominium unit as real property. When you buy a condo, you gain a registered ownership interest in the condominium corporation, which includes your unit and a proportionate share of the common elements.

As a result, the same provincial tax structure applies to condo purchases as to freehold homes.

Many first-time buyers begin with a condo because the entry price is often lower than that of a detached or semi-detached home. This lower price usually results in a lower land transfer tax, even when monthly condo fees are part of the overall budget. Buyers should still calculate the tax early to avoid surprises at closing.

Vacant land, land transfer tax, and HST

Vacant land purchases in Ontario are subject to the land transfer tax. The province calculates the tax on the purchase price using the same tiered formula that applies to homes and condos.

The primary source of confusion is HST. Vacant land may be HST-exempt or HST-taxable depending on how many new lots the seller has created. For example, selling one undivided residential parcel is usually HST exempt, but if the seller creates three or more new lots, HST applies to each lot. Clarifying these scenarios helps buyers understand their total tax obligations beyond the land transfer tax.

Selling one undivided residential parcel is usually HST exempt.

Selling two newly created residential lots is usually exempt.

Once a seller creates three or more new lots, the HST authorities will treat the sale as commercial activity. The seller must charge HST on each lot.

So a parcel divided into four new lots becomes subject to HST, with each lot taxed individually. The same parcel would have been exempt from HST if sold as one parcel or divided into only two lots.

Land transfer tax still applies in these cases. HST depends entirely on lot creation and the seller’s status under CRA rules.

The listing price does not include land transfer tax.

Knowing your land transfer tax in advance helps you plan better and feel more confident at closing, reducing surprises for buyers in Kingston and Eastern Ontario.

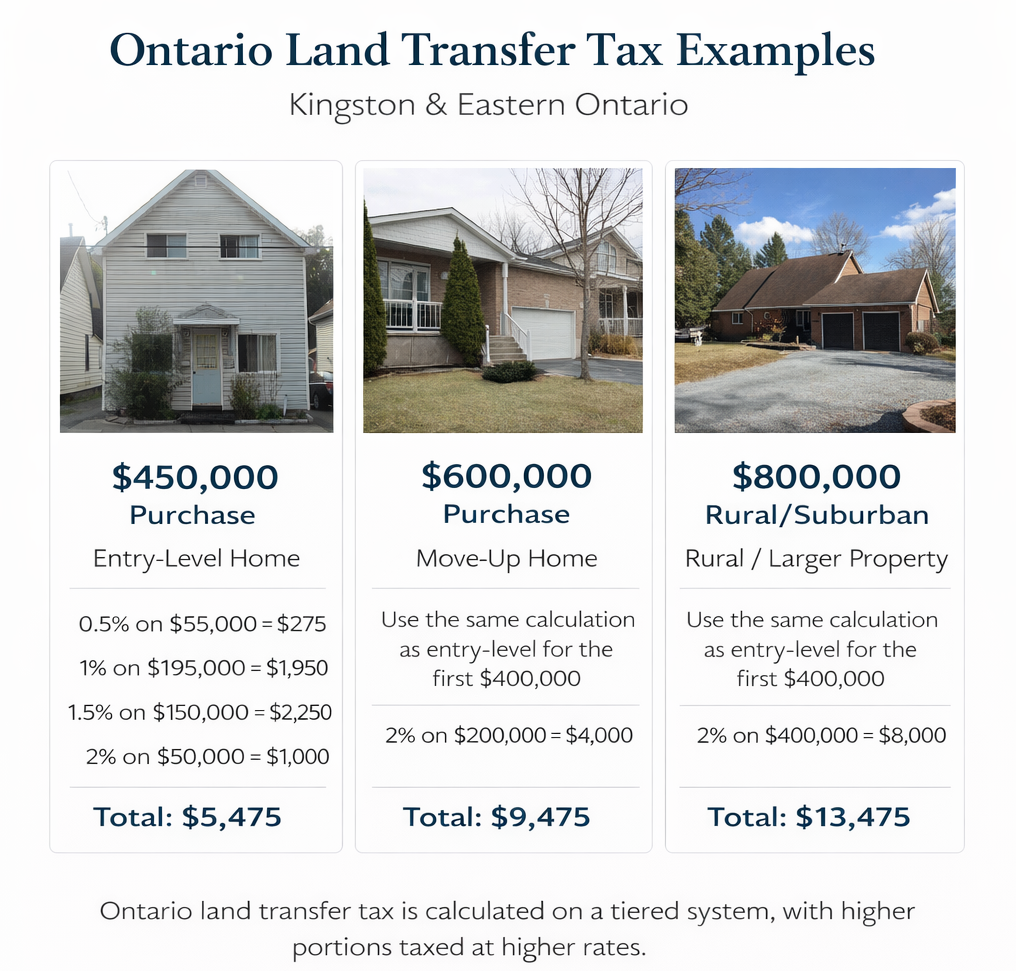

Kingston and Eastern Ontario examples:

First-time buyer rebates

Up to $4,000 in land transfer tax rebates may be available to first-time buyers in Ontario. This can help reduce closing costs, but the rules are strict.

To qualify, a buyer must not have ever owned property anywhere in the world and must not have ever been on title to any property, even if family or estate planning added them. The applicant must intend the home as a principal residence and must meet all program requirements at closing.

Spouse rule

This surprises many buyers. If you have a spouse who has owned a home at any time while they were your spouse, you are not eligible for the rebate, even if your name has never been on the title.

Partial rebate

If you are buying with someone who is not your spouse, the rebate is only available on your share of the purchase. For example, if you purchase a home 50/50 with a parent or a friend, the eligible buyer can claim 50 percent of the maximum rebate, or $2,000.

A common issue

Sometimes people add buyers to a title for family or estate planning reasons. After that occurs, even for a short period, they lose their first-time buyer status, and the rebate becomes inaccessible.

Practical note

No exceptions are made to the rebate eligibility rules. Before joining a title or structuring a joint purchase, it’s wise to verify eligibility.

Use the provincial calculator.

You can test different scenarios using the Ontario estimator:

https://www.ontario.ca/document/land-transfer-tax/calculating-land-transfer-tax

FAQ

Do all property purchases in Ontario require land transfer tax?

Most do. Land transfer tax applies to residential homes, condos, commercial property, and most vacant land. Some narrow exemptions exist under the Land Transfer Tax Act, but they are uncommon in typical real estate transactions.

Does the land transfer tax apply to commercial buildings?

Yes. Commercial, industrial, and multi-residential buildings are subject to land transfer tax at the same rate structure as residential properties, except for the 2.5% rate that applies only to one or two single-family residences priced above $2 million.

Do I pay HST on vacant land?

It depends. A single, undivided residential parcel is usually HST-exempt. Two newly created lots are also typically exempt. When a seller lists three or more new lots, they define commercial activity and must charge HST on each. Land transfer tax still applies in all cases.

Does the land transfer tax apply when buying a condo?

Yes. Even though you do not receive land in the traditional sense, you are still gaining a registered interest in real property. The same land transfer tax structure applies to condo purchases.

Who pays the land transfer tax in Ontario?

The buyer pays the tax. Your lawyer collects the amount and submits it to the provincial government on closing day, once the transfer is registered.

How much is the land transfer tax on a typical Kingston home?

A $450,000 purchase results in approximately $5,475 in land transfer tax. A $600,000 purchase is about $9,475. The exact amount depends on the price and the provincial bracket system.

Do all first-time purchasers automatically receive the land transfer tax refund?

Absolutely not. You must have never owned property globally and never had your name on a property title, regardless of familial or estate circumstances, to be eligible. If your name shows up on a deed, you aren’t a first-time buyer.

Is the land transfer tax included in the listing price?

It’s calculated separately, and they require payment upon closing. Buyers need to factor it into their budgets initially.

📚 Don’t Miss These Guides

Land transfer tax is only one part of the financial preparation required when purchasing a home. These related guides explore budgeting, the buying process, and relocation considerations for buyers navigating the housing market across Kingston and the surrounding Frontenac, Lennox, and Leeds communities.

Kingston and Area Home Buyers Guidebook

A comprehensive overview of the buying process, including financing preparation, property searches, inspections, and closing steps for buyers entering the market throughout the Kingston area and neighbouring Frontenac, Lennox, and Leeds regions.

First Home Purchase: Kingston Area

First-time buyers often face additional questions about financing, conditions, and affordability. This guide walks through the key stages of purchasing a first home and common mistakes to avoid.

Relocating to Kingston and Area 2026

Moving into a new community requires understanding neighbourhood choices, pricing differences, and lifestyle considerations. This guide explains what buyers relocating to Kingston and the nearby Frontenac, Lennox, and Leeds counties should consider before making a move.